Good explanation of why the USA Federal Reserve will NOT take the lead in CBDCs and why China’s Digital Yuan will become important. From NYT, April 26, 2021, full text below and link here: https://www.nytimes.com/2021/04/26/business/economy/fed-digital-currency.html

America’s Federal Reserve says it is in no rush to issue a digital currency, but it is coming under intense and increasing pressure to research and understand the design and potential of digital money.

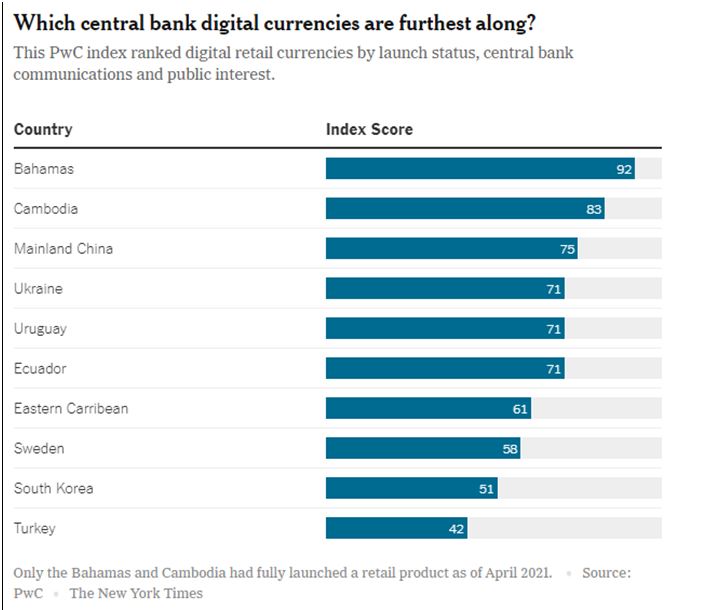

From the Bahamas to China, global central banks are experimenting with digital offerings, fueling concerns on Capitol Hill that the Fed might fall behind the competition. And breakneck innovation in the private sector suggests that the Fed, a key financial regulator, needs to understand budding private digital payment technologies.

Yet huge questions persist about a central bank digital dollar — such as “What problem would this solve?” and “How would it work?” Jerome H. Powell, the chair of the Fed, has been clear that while research is well underway, the Fed has a big responsibility as steward of the U.S. dollar, the world’s dominant currency. It would not issue a digital version of U.S. currency without congressional approval, and it is in no hurry to upend the existing monetary system before it fully understands the consequences.

“Does the public want, or need, a new digital form of central bank money to complement what is already a highly efficient, reliable and innovative payments arena?” Mr. Powell asked at an event in March. It’s a tricky question, and the central bank doesn’t seem to have a clear answer yet. Here’s why.

What is a central bank digital currency?

A central bank digital retail currency is, basically, electronic cash. Like a cryptocurrency such as Bitcoin, it is data-based and doesn’t exist in the physical world, but the similarities end there. Unlike cryptocurrency, it is backed by a government, meaning it is likely to be more universally recognized as “money” — something you can use broadly to buy goods and services and to pay taxes.

How is that different from the money in my Venmo or checking account?

You probably already use digital money. Most workers aren’t paid in physical cash, and many people tend to buy their morning latte with a payment card or app rather than by forking over bills and coins. But the currency underlying paychecks and other day-to-day transactions traces back to the commercial banking system.

America’s money supply is created by a sort of partnership between the Federal Reserve and private banks. The Fed transacts with commercial banks by crediting their accounts with a bank-specific form of electronic central bank money called “reserves.” Commercial banks can swap those reserves for dollar bills and coins — physical central bank money — which their customers can withdraw and spend. Banks also use reserves alongside other capital, like customer deposits, to make loans. When they do so, they create new “private” money that pumps into the financial system in digital form.

That bank-created digital money is what you are using when you swipe your debit card.

Private digital money carries a tiny sliver of risk compared with cash — banks can fail, and deposits are insured only up to $250,000. People intuitively know this: Consumers rush to take out actual dollar bills during times of crisis.

A retail central bank digital currency would be equivalent to green paper bills, because it would have direct backing from the Fed. It would be like reserves — electronic central bank money — but available to the general public.

Who likes this idea, and who doesn’t?

Banks are not keen on the idea of a central bank digital currency. Their lobbyists say the technology would disrupt their business models without offering benefits that the current payment system can’t achieve.

Gregory Baer, the chief executive of the Bank Policy Institute, an industry group, argued in April that banks would not be able to lend against customers’ central bank digital cash holdings the way they lend against customer deposits. That would crimp their ability to make money, so they would need to charge more to carry out everyday banking services, he said. And many analysts have warned that, without safeguards, a central bank digital currency might make it easier for people to pour into digital cash in times of trouble — making the financial system more susceptible to runs.

Researchers recognize the potential for disruption, but some remain enthusiastic.

In an era when cash is going out of style, some central banks see digital cash as a way to make sure the public still has direct access to central bank money. Beyond that, the inception of digital currency might offer a chance to rebuild parts of the payments system from the ground up, allowing for broader financial inclusion, potentially enabling people without traditional bank accounts to send and receive money.

Digital dollars could also have policy applications, perhaps making it easier for the government to put cash straight into consumer accounts during recessions. China has been using its digital currency experiments for such economic purposes.

How far along is the Fed’s research?

Mr. Powell has said researching digital currency is a high priority for the Fed, and lawmakers have kept the pressure on.

Bills proposed by House and Senate Democrats last year would have pushed the Fed to create consumer accounts and deposit central bank digital currency in them as part of the coronavirus relief response. The measures didn’t pass, but they, along with China’s development of a digital currency and private sector efforts from Facebook and others, have helped to light a fire under the Fed’s research and development efforts.

The Federal Reserve Bank of Boston has begun developing experimental digital currency code along with the Massachusetts Institute of Technology, and the Federal Reserve Board is researching the technology and its financial stability implications. The Fed has engaged with international bodies like the Bank for International Settlements in setting out principles for digital currency design.

Lael Brainard, a governor at the Fed, noted last year that deciding to issue a digital dollar would require a lengthy process. Mr. Powell has since said Congress would need to be involved.

For now, research efforts into digital currency “are intended to ensure that we fully understand the potential as well as the associated risks and possible unintended consequences,” Ms. Brainard said.

J. Christopher Giancarlo, a former chairman of the Commodity Futures Trading Commission and an attorney who is now a director of the Digital Dollar Project, a private-sector effort to research an electronic currency, said it was critical to make sure the U.S. kept up when it came to developing the standards and protocols that would govern digital money.

“It’s not about being first, it’s about getting it right — I fully agree with that,” Mr. Giancarlo said, echoing a line Mr. Powell often repeats. “But to be on time, you’ve got to be early.”

Is the U.S. in a race against China?

Emerging markets with big under-banked communities or populations that would benefit from being able to more easily make cross-border payments have been among the earliest adopters of central bank digital currencies. The Bahamas introduced a retail payments digital currency called the Sand Dollar, which is available on iOS and Android, and Thailand is among the places that are far along in researching and developing between-bank, cross-border versions.

But one player in the central bank digital space has earned more headlines than any other: China.

Why the fuss? The world’s second-largest economy has been trying out a pilot version of a digital yuan, putting small amounts of it in consumer accounts in cities including Chengdu and Shenzhen and allowing them to spend it. Researchers at PwC said in an early April report that the digital yuan had the potential to replace cash in circulation and that while “some crucial aspects like an estimated launch timeline remain undisclosed, mainland China is currently believed to be preparing for widespread domestic use” during the Beijing 2022 Winter Olympics.

The question is whether the new technology is going to make the yuan an attractive alternative to other currencies. Chinese central bankers say it is not an effort to supplant the dollar, and Martin Chorzempa, a senior fellow at the Peterson Institute for International Economics, said digitization wouldn’t fix issues that made the yuan unattractive as a reserve currency in the first place — like capital controls, which mean you can’t exchange it easily at all times.

Is Bitcoin coming for the dollar?

Others worry that private-sector innovations like Bitcoin or “stablecoins,” which are backed by a bundle of assets or currencies, could become an attractive alternative to government-created cash if central banks don’t keep up.

Mr. Powell has argued that Bitcoin is more like gold than the dollar. It has value because it’s rare and people want to hold it, so it can even at times be traded for other goods and services, but it is not government-guaranteed money.

But global regulators did slow down Facebook’s stablecoin project, originally known as Libra and now called Diem, because they worried about the potential for money laundering and financial system disruption.

Mr. Powell said in testimony last year that Libra was “a bit of a wake-up call that this is coming fast and could come in a way that is quite widespread and systemically important fairly quickly,” highlighting the “importance of making quick progress.”

If tech companies come to dominate the payment system, that could create privacy and stability issues. In fact, China’s digital yuan was pursued partly in reaction to the rise and dominance of private-sector digital payment platforms like Alipay and WeChat Pay.

A faster or instant payments system, like the FedNow instant payment technology that America’s central bank is now developing, could keep the Fed up to date without changing the system as much as a digital currency would. But digital dollar fans say the point is to prepare for the future — and the future might be central bank digital currency.

“Digital cash, if built in the right way, could be really groundbreaking,” said Neha Narula, who is the director of the Digital Currency Initiative at M.I.T. and is working with the Boston Fed on its project.

Jeanna Smialek writes about the Federal Reserve and the economy. She previously covered economics at Bloomberg News, where she also wrote feature stories for Businessweek magazine. @jeannasmialek